LVMH’s recent activity on Rodeo Drive reflects a broader capital allocation strategy that blurs the lines between brand investment and long-term asset positioning. The conglomerate is aggressively acquiring high-value, flagship real estate in global luxury corridors—most notably Beverly Hills—not only to enhance its experiential retail presence but also to consolidate long-term margin protection and balance sheet control. This dual strategy mirrors the thinking of institutional real estate investors and top-tier brand strategists alike. Below, I evaluate this move through both strategic and financial lenses.1

Strategic Overview: Why Ownership over Leasing?

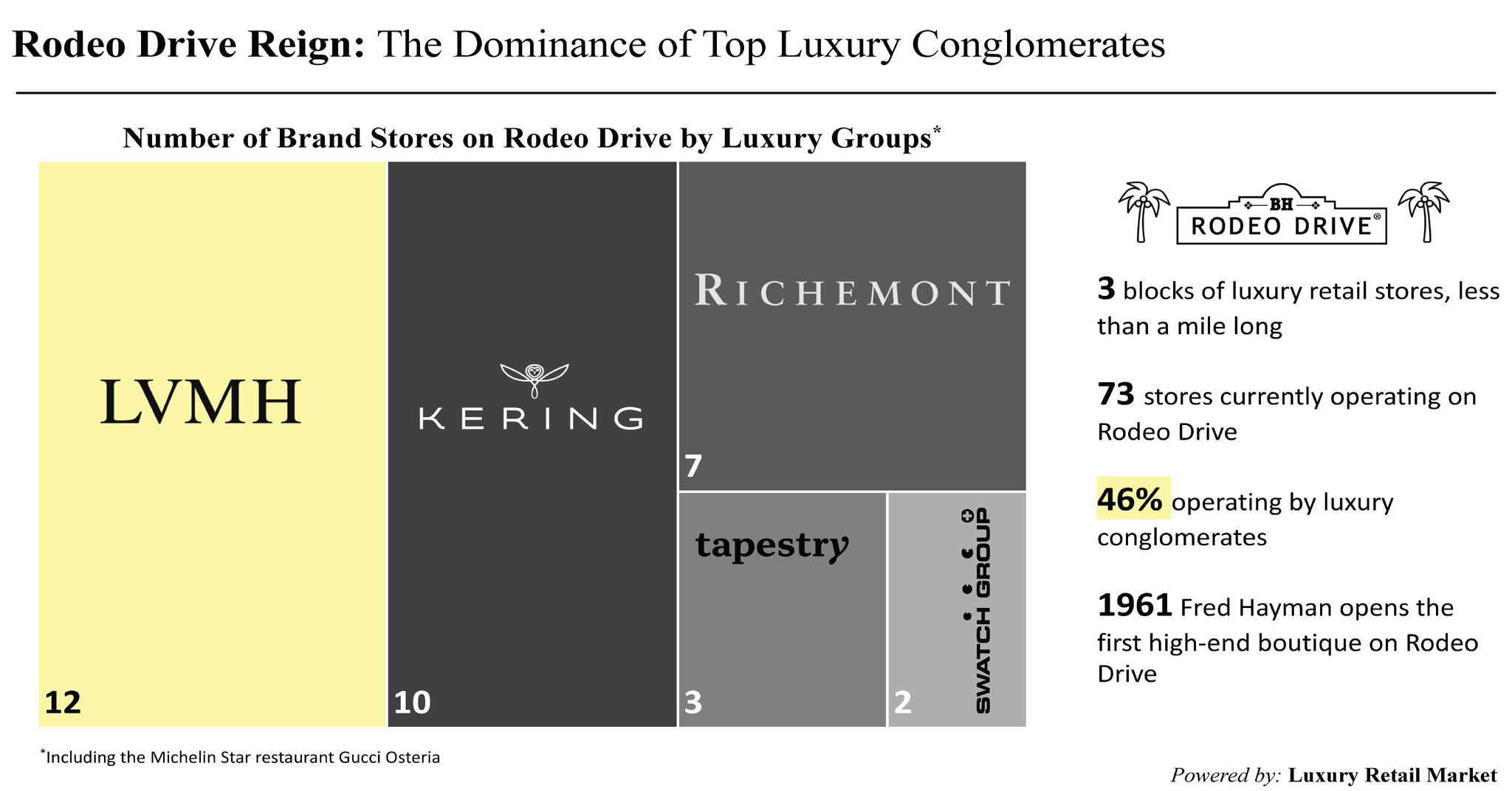

For a luxury group like LVMH, acquiring flagship real estate offers a strategic hedge against market volatility, rent escalation, and inconsistent landlord standards. Ownership provides multi-decade brand control over key physical touchpoints. In a category where the physical store is both showroom and stage, controlling the real estate becomes synonymous with protecting the brand.

On the upside, owning:

- Locks in operating costs, neutralizing rent inflation risks (Rodeo Drive rents exceed $1,100/sq. ft. in 2024)

- Secures strategic corners in global luxury corridors

- Enables brand-integrated architectural investment, maximizing brand impact and customer immersion

- Converts rent expense into capitalized assets, lifting EBITDA and free cash flow over time

On the downside:

- Capital outlay is significant, reducing ROIC in the near term

- Fixed asset ownership reduces agility in dynamic retail markets

- Balance sheet carries depreciation and financing liabilities, affecting net income optics

- Opportunity cost: capital deployed into real estate may limit flexibility elsewhere (e.g., M&A, digital, logistics)

The decision calculus depends on LVMH’s capital structure and appetite for duration risk—both of which are robust. The group’s liquidity and operating margins enable it to treat flagship locations as strategic, yield-adjusted real estate holdings.

P&L and Capital Modeling: Own vs. Lease Economics

To better visualize the financial rationale behind LVMH's ownership strategy, I bifurcated a Rodeo Drive flagship into a two-part framework: