From Hollywood playgrounds to conglomerate real estate warfare, the Southern California luxury retail market represents a highly complex matrix of extreme wealth concentration, historic cultural cachet, and aggressive commercial real estate (CRE) capitalization.

Spanning from the ultra-exclusive enclaves of Montecito to the high-density, volume-engineering hubs of Orange County, this regional ecosystem serves as the definitive testing ground for global luxury conglomerates.

To understand the current structural realignment of this market—where heritage brands are actively transitioning from passive tenants to aggressive real estate holding companies—one must first examine the historical and cultural foundations that transformed Southern California into a global luxury zenith.

This is the first chapter from our 6-Chapter research series titled: The Structural Realignment of Luxury Retail & Commercial Real Estate. The structure of this series is as follows: Preface, Foreword, Prologue, Chapters 1-6 and Epilogue.

The Preface, Foreword and Prologue establishes the macro foundation for this research series by analyzing the forces that are reshaping the economics, and geography of luxury retail.

If you're just joining us, you can start by reading the Preface of the series below:

The Genesis of the Apex: Rodeo Drive’s Historical Architecture

Before Rodeo Drive commanded the highest leasing premiums in the United States outside of New York, it was an unassuming residential and local commercial street. Its transformation into an international theater for brand equity was catalyzed in the late 1960s and 1970s by a cadre of visionary independent retailers who fundamentally understood that luxury was an immersive experience rather than a mere transaction.

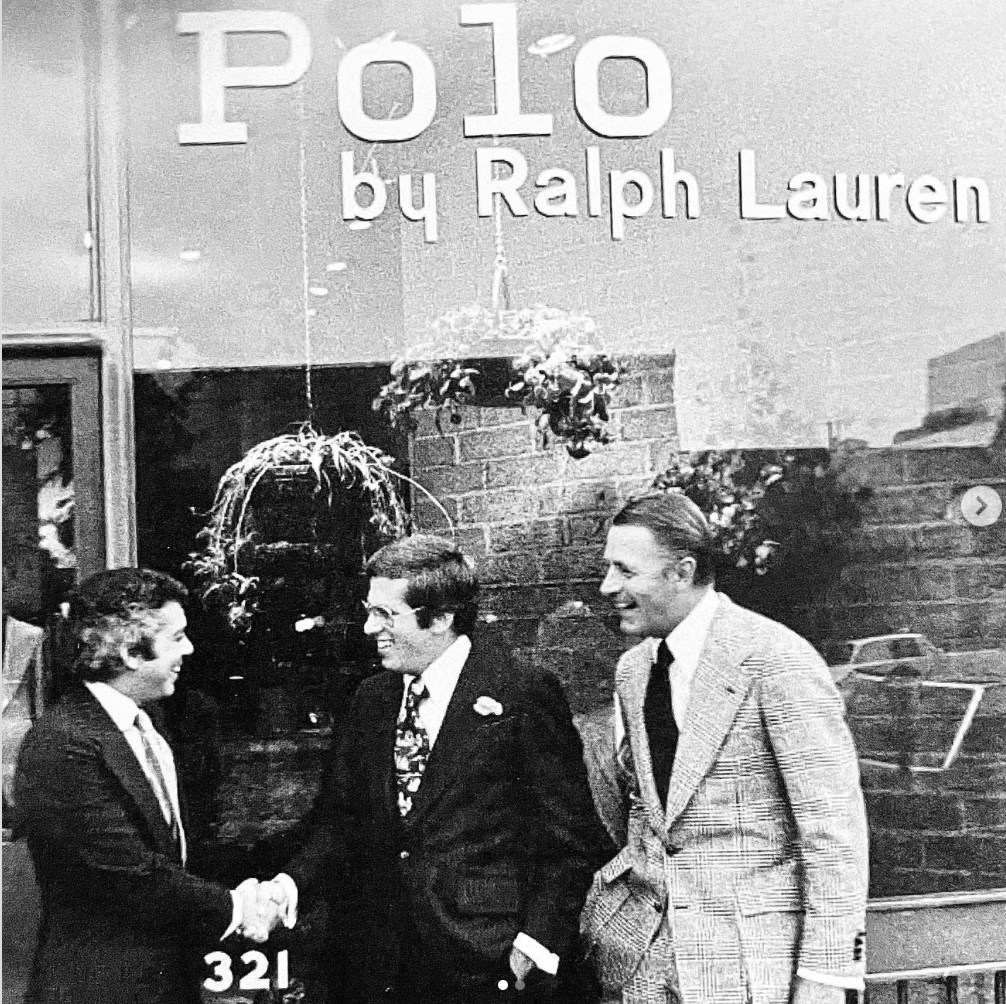

A pivotal moment in this evolution occurred in 1971 when Jerry Magnin, a scion of the legendary I. Magnin retail family opened the first-ever freestanding Polo Ralph Lauren store on Rodeo Drive. This bold franchising maneuver established the viability of the standalone, single-brand boutique, diverging from the traditional multi-brand department store model.

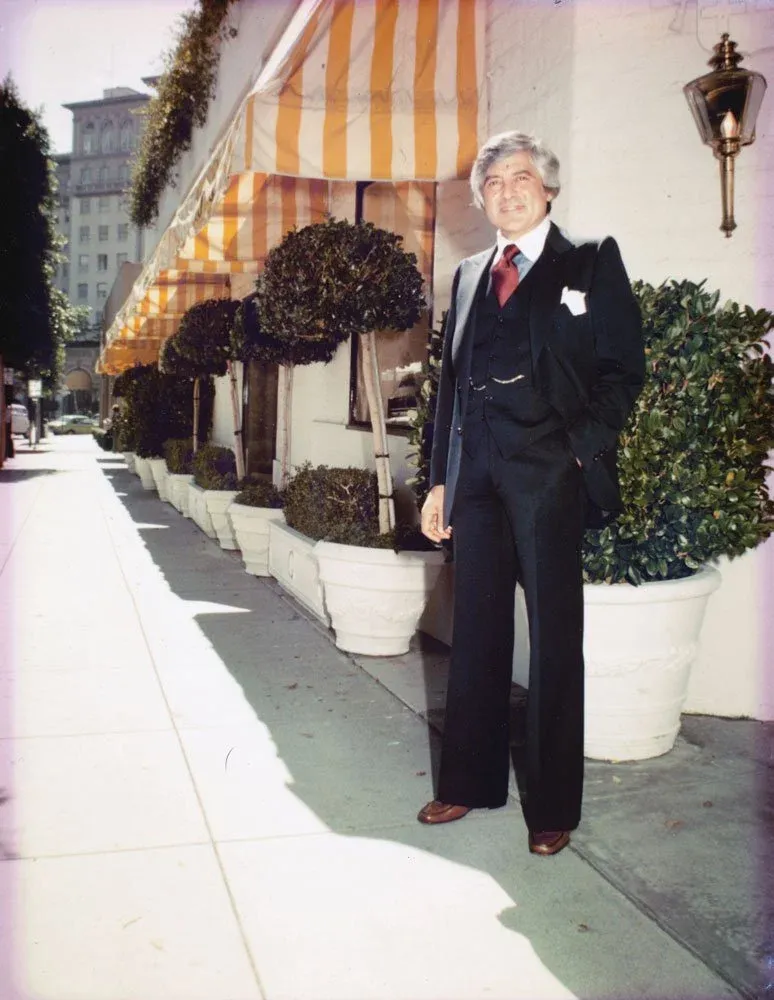

Concurrently, Fred Hayman revolutionized spatial hospitality with the opening of Giorgio Beverly Hills. Hayman engineered a club-like atmosphere, outfitting hi s boutique with a functioning bar, a pool table, a reading area, and an oak fireplace, famously delivering finished garments to clients' homes via Rolls-Royce. This experiential operational model yielded astonishing financial metrics for the era, with Giorgio reportedly generating $1,000 per square foot in 1978.

This foundation of extreme, localized exclusivity was further cemented by Bijan Pakzad, whose eponymous menswear boutique operated strictly by appointment, catering exclusively to a clientele he characterized as earning upwards of "$100,000 a month". Together, Magnin, Hayman, and Pakzad established the experiential and psychological parameters of Rodeo Drive, creating a cultural halo that European heritage brands would eventually cross the Atlantic to capture.

The Modern Rodeo Drive: A Billion-Dollar CRE Battleground

Today, the experiential groundwork laid by those pioneers has been institutionalized and weaponized by global luxury conglomerates. Operating with near-zero functional vacancy, Rodeo Drive commands average leasing rates of approximately $1,000 to over $1,100 per square foot. In this hyper-competitive environment, the strategic mandate has shifted from securing leases to executing outright fee-simple acquisitions.

The rationale is rooted deeply in corporate finance: by purchasing prime real estate outright, luxury conglomerates effectively neutralize the perpetual operating liability of exorbitant rent escalations, converting those costs into capitalized, appreciating assets that structurally inflate reported EBITDA. This lease-versus-own dynamic reached a historic crescendo in February 2026, when Hermès shattered Beverly Hills retail records by acquiring two adjoining storefronts at 338 North Rodeo Drive for a staggering $400M (brokered by Jay Luchs of Newmark).

Simultaneously, LVMH is acting as a de facto urban planner, consolidating massive contiguous blocks to control the consumer journey in its entirety. The conglomerate recently secured unanimous approval from the Beverly Hills Planning Commission for a colossal, 100,000-square-foot mega-flagship designed by Frank Gehry.

For a comprehensive financial teardown of how this specific spatial capitalization strategy protects corporate margins, industry analysts are highly encouraged to read our definitive LRM report below:

Furthermore, this real estate warfare extends aggressively into the hard-luxury sector, where margin profiles justify immense capital expenditures. To understand the architectural maneuvering within this high-yield category, readers should explore the LRM strategic analysis, Tiffany Just Declared War on Rodeo Drive—And Cartier Is in the Crosshairs, which details the battle for the street's most lucrative intersections.

The Desert Liquidity Migration: Palm Springs to El Paseo

The cultural magnetism of Southern California luxury has historically followed the migratory patterns of its celebrity and socialite elite. By the mid-20th century, the Coachella Valley had established itself as the ultimate desert playground for Hollywood executives and political dignitaries. Recognizing this concentrated, seasonal liquidity, luxury retail followed the rooftops. In the 1960s, the Desert Inn Fashion Plaza in downtown Palm Springs became the epicenter of desert luxury, anchored by prestigious full-line stores including I. Magnin and Saks Fifth Avenue.

However, as regional wealth expanded eastward, the retail center of gravity shifted definitively toward Palm Desert. El Paseo emerged as the shopping destination, systematically drawing luxury anchors away from Palm Springs. Despite its historical dominance, the El Paseo corridor is currently navigating the broader macroeconomic headwinds facing legacy department stores. In early March 2026, Saks Global initially announced the permanent closure of its 50,000-square-foot anchor store at The Gardens on El Paseo as part of a massive national Chapter 11 bankruptcy restructuring. However, in a stark reversal mere weeks later, Saks Global rescinded the closure, designating the Palm Desert location as a critical component of its "go-forward" portfolio.

This strategic pivot reveals profound insights into both Saks Global’s resort strategy and the underlying economics of Palm Desert. By successfully renegotiating lease terms with landlord Simon Property Group to maintain operations, Saks demonstrated a ruthless commitment to markets exhibiting a "high concentration of luxury shoppers" capable of sustaining highly attractive profitability models.

The reversal effectively proves that the Coachella Valley's seasonal influx of ultra-high-net-worth residents and international tourists remains an indispensable liquidity engine. Furthermore, from a commercial real estate perspective, this negotiation highlights a rare instance of tenant leverage: institutional landlords actively recognize that retaining a heritage luxury anchor is vital to preserving broader asset valuations and stabilizing high-end co-tenancy on El Paseo.

Micro-Footprints and Mega-Scale: Montecito and Orange County

As luxury retail bifurcates, Southern California provides the definitive case studies for both the micro-footprint hospitality model and the mega-scale volume engine.

In Montecito, the Rosewood Miramar Beach resort—a Rick J. Caruso development—perfectly encapsulates the high-conversion, captive-audience model. Operating within a 16-acre pristine beachfront property, the resort features hyper-curated, micro-boutiques from elite houses such as Bottega Veneta, Brunello Cucinelli, and the newest Chanel fashion boutique. By embedding retail within an ultra-luxury hospitality environment, these brands capture continuous, high-net-worth liquidity without the massive overhead of high-street flagships.

Conversely, South Coast Plaza in Costa Mesa serves as the absolute zenith of operational scale. Generating annual taxable sales of ~$2.5B and attracting 24M visitors, it is the highest-grossing planned retail center in North America. The property has successfully shielded itself from the broader "mall apocalypse" by functioning as an impenetrable luxury fortress.

Recent capital markets data highlights the center's immense leasing velocity, including a massive 30,500-square-foot lease executed by Bulgari, Cartier, and Gucci, as well as nine new luxury store debuts tracked between 2024 and 2025.

The Mixed-Use Horizon: San Diego's Westfield UTC and Fashion Valley

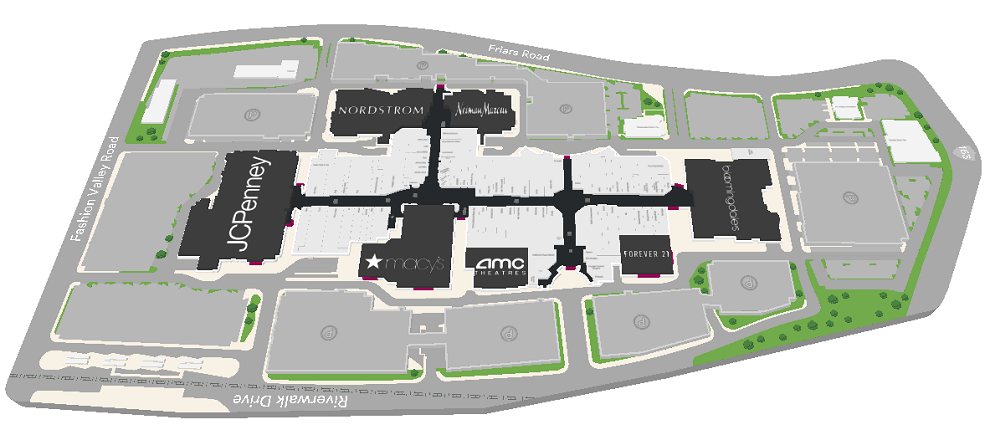

The Southern California analysis concludes in San Diego, a market that is undergoing a profound geographic and demographic shift in its luxury center of gravity. For decades, Simon Property Group's Fashion Valley served as the undisputed luxury destination for the region.

However, over the past decade, Unibail-Rodamco-Westfield (URW) has successfully engineered a market coup at Westfield UTC, functionally eclipsing Fashion Valley as an ultra-luxury retailer destination. This transition is most starkly evidenced by heritage megabrands migrating their physical footprints; notably, Hermès closed its Fashion Valley location to open an expansive new boutique at UTC. This momentum is further compounded by the introduction of a standalone Chanel fashion boutique and the arrival of Italian ultra-luxury house Loro Piana, their first retail stores in San Diego.

This geographic reallocation of luxury capital is deeply intertwined with shifting consumer behavior and international liquidity. A primary economic engine for San Diego's luxury sector is the robust cross-border wealth generated by Mexican nationals. Increasingly, this affluent demographic has concentrated its capital in La Jolla, driving strong demand for luxury second homes in the immediate vicinity of UTC. Consequently, luxury retail is merely following the rooftops.

Historically, La Jolla itself functioned as the localized luxury hub. “The Village,” in La Jolla, was the neighborhood's high-end shopping district that previously hosted prominent anchors like Saks Fifth Avenue (which attempted to enter the market twice). During the early 2000s and 2010s, brand consolidation shifted this prestige to Fashion Valley's mega-mall format. Today, the luxury epicenter has returned to the La Jolla perimeter, but the paradigm has shifted from neighborhood street-fronts to highly controlled, experiential mall environments.

This battle highlights the divergent strategic frameworks of two real estate titans: URW and Simon Property Group. URW's strategy at Westfield UTC aligns with their refined "moins, mais mieux" (less, but better) corporate mandate, focusing on a highly curated, ultra-luxury portfolio. They have transformed UTC into a resort-inspired destination, integrating Michelin-rated dining, health and wellness centers, and the 23-story Palisade luxury residential tower directly into the retail footprint.

Conversely, Simon is executing a radical structural evolution at Fashion Valley to reclaim market share.

“We’re excited about this next phase of Fashion Valley as we continue to reinvest and add a walkable, livable lifestyle community that is intertwined with handpicked luxury brands that can only be found here.”

—Mark Silvestri, President of Development at Simon

By strategically demolishing legacy anchors like JCPenney, Simon is partnering with AMLI Residential to build 850 luxury multifamily residences, aiming to create a self-sustaining, closed-loop community around its retail core.

Ultimately, Westfield is curating an ultra-luxury hospitality ecosystem, while Simon is engineering a high-density, mixed-use residential village.

Key Takeaways and Strategic Insights

The Southern California luxury retail sector is no longer merely a collection of high-end shopping districts; it is a sophisticated, multi-billion-dollar asset class. From the record-breaking $400M real estate acquisitions on Rodeo Drive to the ~$2.5B in operational machinery at South Coast Plaza, the market dictates that physical stores must function as heavily capitalized bastions of brand equity.As we analyze this ecosystem, three critical insights emerge:

- Real Estate as the Ultimate Operational Moat: The era of passive tenancy is ending. Elite conglomerates are actively converting exorbitant rent liabilities into capitalized, yield-generating assets. In hyper-competitive corridors, outright ownership is increasingly the only absolute hedge against supply constraints.

- The Barbell Strategy is Physical Reality: Retail success is polarizing between massive operational scale (the volume engines of South Coast Plaza) and hyper-intimate, hospitality-integrated micro-footprints (the captive audience model at Rosewood Miramar).

- Capital Follows Liquidity Migration: As localized wealth shifts, so does the architectural deployment of capital. The historic retail migration from Palm Springs to El Paseo and the current mixed-use, residential-retail transformations in San Diego prove that physical luxury must be highly agile in tracking demographic wealth concentrations.

As we look ahead, the foundational blueprint established in Beverly Hills and its surrounding nodes serves as the critical lens through which we will evaluate the rest of the North American luxury landscape.

This structural shift prompts a critical question for market strategists and real estate professionals alike:

Will the aggressive capital expenditure in hard-asset flagships insulate these mega-brands from the impending macroeconomic softening, or are they building beautiful monuments to a bygone era of unchecked consumer liquidity?

Join the Conversation

We invite you to engage with this ongoing structural realignment. Which Southern California node do you believe possesses the most resilient long-term yield profile?

Share your insights in the comments below.

If you're not yet, subscribed to LRM, click here for full access to our proprietary models and financial teardowns, and follow the 6-Chapter series as we prepare to dissect the tech-driven wealth and urban revitalization of Northern California in Chapter 2.