The Paradigm of Experiential Alpha and Capital Consolidation

Following a historic super-cycle of value creation spanning from 2019 to 2023—an era wherein the personal luxury goods market achieved record profitability driven largely by relentless price increases and scale-driven volume gains—the industry currently faces a complex matrix of systemic headwinds.1 As the market transitions into 2026, navigating this landscape requires a sophisticated synthesis of retail strategy, institutional capital allocation, and advanced operational execution. The traditional paradigms of passive real estate leasing and purely transactional retail have been rendered structurally obsolete. In their place, an environment defined by strategic asset ownership, hyper-personalized client engagement, and architecturally immersive "mega-flagships" has emerged as the definitive standard for preserving and compounding brand equity.

This Preface serves as a foundational theoretical analysis and precursor to the upcoming comprehensive 6-Chapter research series titled: The Structural Realignment of Luxury Retail & Commercial Real Estate. This forthcoming series will exhaustively explore the prime luxury retail markets in the United States, analyzing the specific street-level economics and architectural battlegrounds of Beverly Hills, San Francisco, Chicago, Dallas, New York City, and Miami. By applying a multidisciplinary framework, this report dissects the forces reshaping the luxury retail real estate ecosystem. The analysis traverses the macroeconomic currents of the global fashion industry, the capitalization and yield dynamics of prime commercial real estate, and the operational bifurcation of retail formats. Specifically, it contrasts the monumental scale of global flagship operations with the extreme intimacy of private, appointment-only salons and curator-led specialty boutiques.

The convergence of these economic, technological, and social forces has left luxury conglomerates and private equity stakeholders navigating a highly contested environment. Chronic supply shortages in prime retail corridors, evolving consumer priorities centered on well-being and experiential resonance, and the persistent threat of geopolitical and tariff turbulence demand an aggressive recalibration of capital deployment strategies.2 Through this analytical lens, this report establishes the critical baseline necessary for understanding the hyper-competitive luxury markets that dictate the future of the physical retail experience.

Macro Overview of the Luxury Goods and Fashion Industry

The Recalibration of Growth and the Macroeconomic Headwinds of 2026

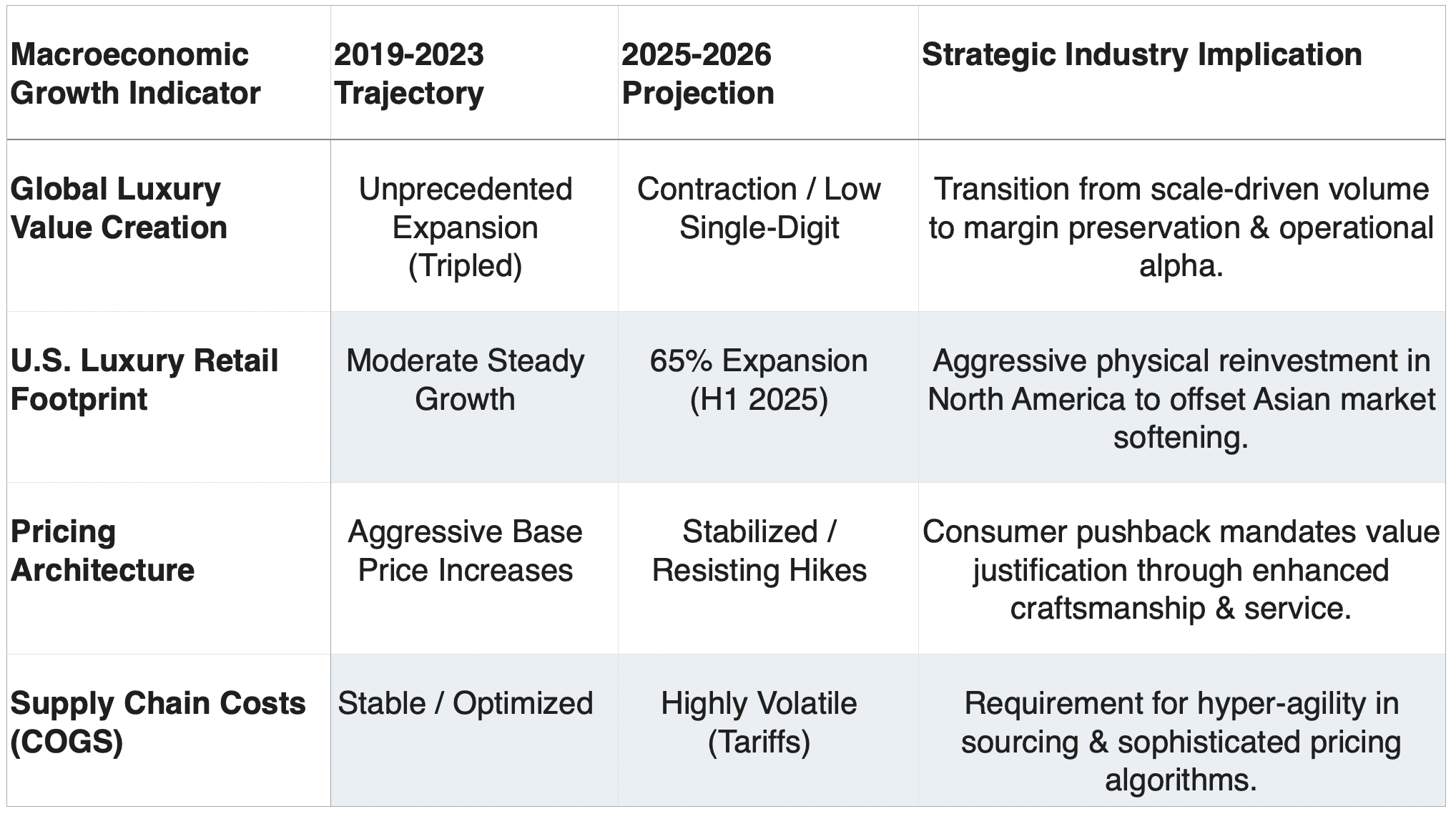

The global luxury and fashion industry is transitioning through a critical phase of strategic renewal, stabilization, and margin defense. Between 2019 and 2023, the luxury sector achieved a remarkable 5% CAGR, outperforming global equities as economic profit nearly tripled and megabrands leveraged their immense scale to drive unprecedented desirability.1 However, the economic reality of 2025 and 2026 dictates a stark return to normalized, low-single-digit growth.2 For the first time since 2016, excluding the pandemic anomaly of 2020, luxury value creation has experienced contraction, forcing conglomerates to confront stalled growth engines and severe consumer pushback against relentless, inflation-mimicking price hikes.1

Heading into 2026, macroeconomic volatility and shifting trade maps remain the primary operational concerns for corporate boards. Tariff turbulence, specifically enacted and proposed United States tariffs, has emerged as the single most significant hurdle for luxury executives, pushing up costs across the global value chain and forcing brands to rapidly adjust their sourcing logistics and pricing architectures.2 For instance, major fashion holding companies such as Capri Holdings have explicitly anticipated significant increases in the cost of goods sold—projecting upwards of an $85M impact for fiscal year 2026—solely due to these tariff environments.5 Consequently, the psychological disposition of the industry is cautious; 46% of fashion executives expect global industry conditions to worsen in 2026, representing a notable increase from the 39% who held pessimistic outlooks the previous year.2 Concurrently, prominent luxury conglomerates, including LVMH and Kering, reported highly challenging revenue environments in the first half of 2025, reflecting broader consumer hesitancy and normalized household budgeting under persistent cost-of-living pressures.4

Despite these pronounced macroeconomic headwinds, the United States remains a critical bright spot and the primary target for aggressive capital reinvestment by European heritage brands. Luxury conglomerates have strategically chosen not to allow top-line volatility to derail long-term physical infrastructure expansion strategies. In a striking display of market confidence, newly opened luxury retail square footage in the U.S. increased by 65% in the first half of 2025 (see Table 1.) compared to the same period in 2024, forcefully rebounding from a 14.3% contraction the prior year.2 This massive injection of retail capital expenditures underscores a foundational industry belief: physical retail, specifically street-level flagships, remains the paramount engine of luxury revenue generation, brand equity solidification, and experiential dominance.5

Table 1. Macroeconomic Review

Shifting Consumer Typologies: The Well-Being Era, the AI Shopper, and the Hard Luxury Boom

The qualitative nature of luxury consumption is evolving as rapidly as the macroeconomic environment that governs it. The affluent consumer of 2026 demands profound emotional connection, brand purpose, and curated experiences that transcend the basic transactional acquisition of physical goods.4 This profound behavioral shift has ushered in the "Well-being Era," wherein high-net-worth individuals are redirecting vast sums of discretionary spending toward non-fashion categories and immersive experiences that cater to holistic health, physical longevity, and psychological enrichment.2 Brands that successfully integrate these priorities into multi-dimensional "third spaces"—hybrids of retail, hospitality, and elite wellness—are capturing outsized market share and dramatically extending in-store dwell times.

Technological disruption is further altering the traditional path to purchase, creating entirely new paradigms of consumer interaction. The integration of artificial intelligence within the luxury sector has moved far beyond generative imagery and supply chain optimization, rapidly entering the realm of "agentic commerce".2 In 2026, the industry is witnessing the ascension of the autonomous "AI Shopper"—highly sophisticated algorithmic agents capable of monitoring global pricing discrepancies, assessing limited-edition product availability, and executing immediate purchases on behalf of time-poor, ultra-high-net-worth clients.2 To remain visible to these non-human buyers, luxury brands are being forced to re-architect their digital and e-commerce infrastructures entirely, transitioning away from traditional SEO toward generative engine optimization (GEO) and API-accessible inventory protocols.2

Simultaneously, a distinct bifurcation in product category performance has materialized within the physical stores. While aspirational leather goods, footwear, and entry-level ready-to-wear apparel face softening demand elasticities, "hard luxury"—specifically fine jewelry and haute horlogerie—is experiencing a monumental and sustained boom. Empirical data forecasts that jewelry will be the fastest-growing category in fashion by unit sales in 2026, expanding at more than four times the rate of standard clothing.2 Benefiting from a consumer base that fundamentally prioritizes self-expression, significant self-gifting, and long-lasting, wealth-preserving investments over transient seasonal trends, jewelry has defied the broader luxury slowdown.2 Hard luxury is cementing its role as the absolute centerpiece of modern luxury portfolios, prompting conglomerates to reallocate prime real estate square footage toward expansive, high-security jewelry salons.

For a granular analysis of how this specific shift toward hard luxury is physically reshaping prime retail corridors, read our comprehensive research piece below:

That report meticulously details the strategic maneuvering and architectural expansion occurring within the fine jewelry sector.

Macro Overview of Commercial Real Estate for the Luxury Sector

Capital Markets, Supply Constraints, and Real Estate as a Safe Haven

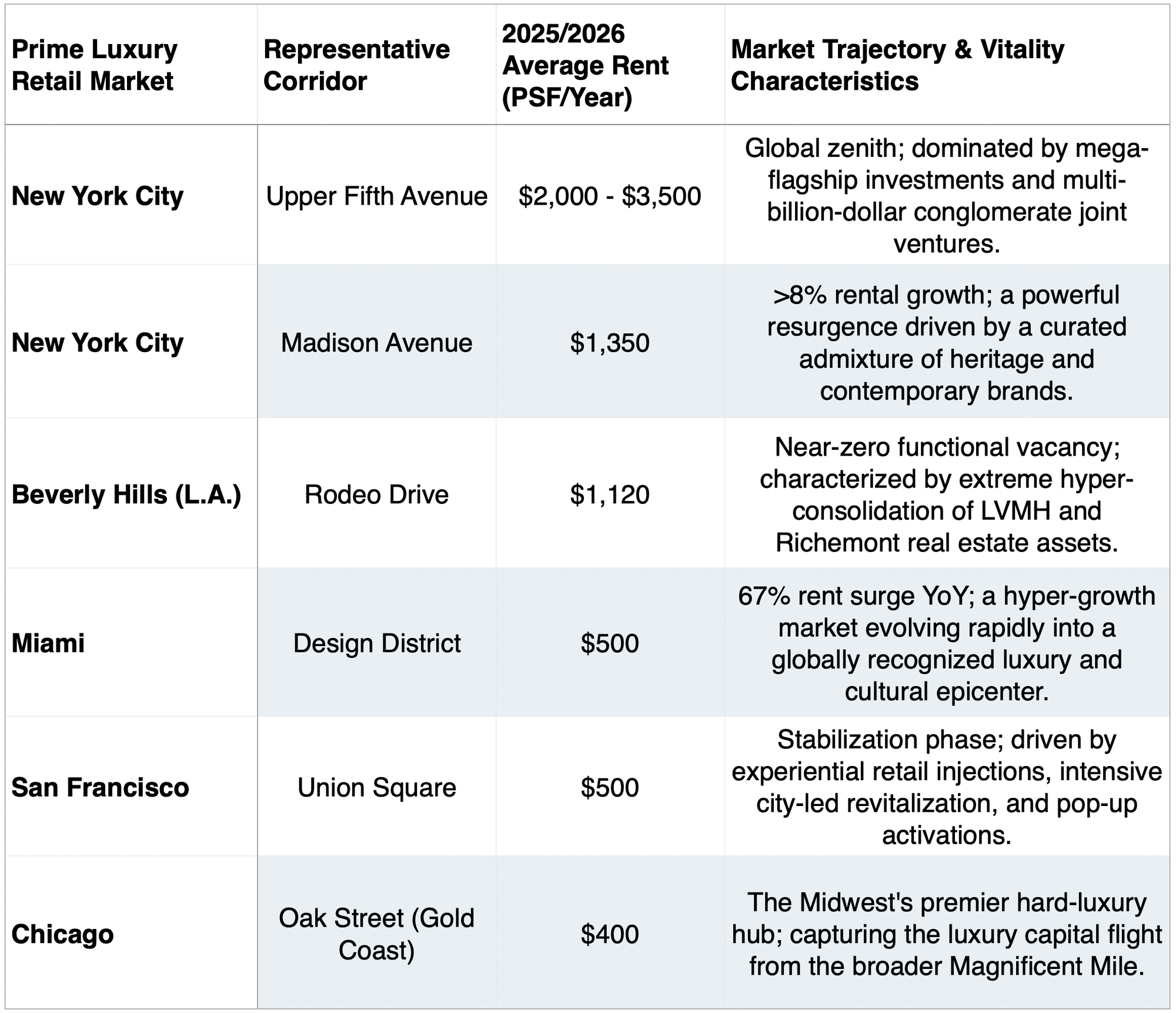

The commercial real estate (CRE) landscape for prime luxury retail is currently defined by severe supply constraints, robust tenant demand, and a highly competitive, shifting capital market dynamic (see Table 2.). While broader commercial real estate sectors, such as traditional suburban office spaces and commodity retail, face structural overhangs and existential crises regarding functional obsolescence, premium high-street retail has demonstrated remarkable resilience and yield stability.10 Following a period of muted transaction volumes in 2024, driven by elevated sovereign interest rates and wide bid-ask spreads, the 2026 capital markets environment is characterized by selective acceleration, stabilizing cap rates, and significantly improved price discovery across top-tier assets.11

A primary driver of elevated retail pricing and sustained landlord leverage is the chronic, structural lack of new construction. New retail development starts remain near historic lows, having precipitously fallen over 50% quarter-over-quarter in mid-2025 to a mere 4.9 million square feet nationally.5 Rising construction costs, exacerbated by persistent inflationary pressures and skilled labor shortages, continue to outpace potential rental growth in secondary and tertiary markets, rendering speculative retail development economically unviable.5 Consequently, luxury retailers are forced into intense, bidding-war competition for existing, high-quality Class-A assets in established prime urban corridors. This scarcity premium ensures that high-street availability remains critically low, empowering institutional landlords with significant pricing leverage and driving sustained rental appreciation across the board.14

From an institutional investment banking perspective, luxury real estate has definitively cemented its status as a premier "safe haven" asset class.10 Ultra-high-net-worth individuals, elite family offices, and sovereign wealth funds are increasingly utilizing prime retail real estate as a stabilizing, income-generating cornerstone within globally diversified portfolios, effectively shielding vast reserves of capital against geopolitical volatility and inflationary erosion.16 The convergence of luxury brands seeking absolute operational control and institutional capital seeking secure, bond-like yields has resulted in a highly competitive, over-capitalized market environment where physical property is viewed simultaneously as a financial hedge and a core operational requirement.17

Table 2. Prime Luxury Retail Overview

The Lease vs. Own Dichotomy: Capital Allocation and EBITDA Optimization

Perhaps the most consequential strategic shift within the luxury commercial real estate sector is the aggressive, industry-wide transition from traditional leasing models to outright property ownership by elite luxury conglomerates. For decades, luxury brands operated under an asset-light, operational philosophy, utilizing long-term leases to maintain capital fluidity and geographic agility. However, the current macroeconomic climate—characterized by exorbitant rent hikes, inconsistent landlord maintenance standards, and the absolute necessity for total architectural control—has catalyzed a massive reallocation of corporate capital toward direct real estate acquisition.

By purchasing prime real estate outright, luxury conglomerates effectively neutralize the threat of exorbitant, market-rate rental expenses, converting a perpetual operating liability into a capitalized, appreciating asset. This strategy acts as a powerful, structural hedge against localized inflation and aggressive rent escalations in highly supply-constrained corridors like Rodeo Drive and Fifth Avenue. Furthermore, ownership grants these brands "multi-decade control" over their physical environments, enabling the execution of massive, capital-intensive architectural projects—such as multi-story flagship temples featuring integrated hospitality, culinary concepts, and museum-grade curation—that would be functionally impossible, or financially unjustifiable, to execute on leased land.

To fully comprehend the magnitude of this financial pivot, industry strategists are highly encouraged to review our definitive research report below:

That report meticulously dissects how the conglomerate converts astronomical rent expenses into capitalized real estate assets, thereby securing an insurmountable competitive operational moat.

Conglomerate M&A and Strategic Real Estate Joint Ventures

The relentless pursuit of prime real estate ownership has triggered a wave of sophisticated mergers, acquisitions, and joint ventures among the dominant luxury players, most notably LVMH, Kering, Chanel, and Richemont. Recognizing that prime high-street real estate is a strictly finite resource, these conglomerates are engaging in a multi-billion-dollar "arms race" to secure the absolute best intersections globally.

When outright acquisition strains corporate liquidity or concentrates an unacceptable level of risk on the balance sheet, conglomerates are increasingly deploying highly innovative financial structuring. A paramount example of this strategy is Kering's recent, landscape-altering transaction on New York's Fifth Avenue. After acquiring the expansive, multi-level retail asset located at 715-717 Fifth Avenue for an astonishing $963M in 2024, Kering swiftly executed a joint venture agreement with the global private investment firm Ardian.25 By selling a 60% majority equity stake to Ardian for $690M (which valued the asset at $900 million), Kering successfully monetized the real estate, vastly enhanced its short-term financial flexibility, and retained a powerful 40% equity stake, all while perpetually securing a long-term, ultra-prime location for its flagship operations.25 This sophisticated, multi-layered maneuver perfectly exemplifies how modern luxury houses are blending private equity capitalization tactics with localized retail strategy to optimize their balance sheets without sacrificing high-street dominance.

As a 501(c)(3) nonprofit organization, we are funded by the community. Every contribution—big or small—from our members, industry peers, clients, & enthusiasts, helps fuel our mission.

Join the Conversation and Follow the Series

The 2026 luxury retail and commercial real estate landscape is structurally unforgiving and highly complex. As conglomerates execute multi-billion-dollar real estate acquisitions to fortify their brand equity and heavily manipulate EBITDA margins, the barriers to entry in prime corridors have never been more formidable. Concurrently, the sophisticated consumer demand for hyper-personalized, highly private, and emotionally resonant shopping experiences is forcing a fundamental, ground-up rethink of the physical retail store.

Next week will continue the 6-Chapter research series with the Foreword section by Ashley Itliong, global luxury real estate strategist and a contributor here at LRM. The structure of this series is as follows: Preface, Foreword, Prologue, Chapters 1-6, and Epilogue.

We invite industry leaders, financial analysts, brand strategists, and retail enthusiasts to comment below with your perspectives on the shifting dynamics of luxury real estate.

Subscribe to the LRM and follow our publications to ensure you do not miss Chapter 1: The Rodeo Drive Paradigm

In addition to direct industry experience and internal market data from LRM Intelligence, our in-house research center, this report cites the following data sources and articles:

References

- The State of luxury goods in 2025 - McKinsey, accessed March 2, 2026, https://www.mckinsey.com/industries/retail/our-insights/state-of-luxury

- The State of Fashion 2026: When the rules change | McKinsey, accessed March 2, 2026, https://www.mckinsey.com/industries/retail/our-insights/state-of-fashion

- Global Real Estate Outlook - JLL, accessed March 1, 2026, https://www.jll.com/en-us/insights/market-outlook/global-real-estate

- Luxury and Fashion 2026: Navigating Uncertainty, Embracing Change and Leading with Purpose - Euromonitor International, accessed April 2, 2026, https://www.euromonitor.com/article/luxury-and-fashion-2026-navigating-uncertainty-embracing-change-and-leading-with-purpose

- JLL Luxury retail report 2025.pdf, https://drive.google.com/open?id=1G8FyV0cJ8WL14tg0veeG-Iv2FpdwuZaf

- Physical Stores in Luxury Retail Still Drive Growth | P&C Global, accessed March 1, 2026, https://www.pandcglobal.com/research-insights/why-physical-luxury-retail-stores-still-drive-growth/

- Experience Hubs in Retail: Redefining Luxury Boutiques for a New Era - Thomas Wieringa, accessed April 2, 2026, https://www.thomaswieringa.com/post/rethink-the-role-of-retail-luxury-boutiques-as-experience-hubs

- Will This be the Most Expensive Store Ever Built on Rodeo Drive? https://luxuryretailmarket.org/most-expensive-luxury-retail-store/

- Tiffany Just Declared War on Rodeo Drive—And Cartier Is in the Crosshairs, https://luxuryretailmarket.org/tiffany-vs-cartier-rodeodrive/

- Bend, Not Break: Investing in Real Estate Amid Economic Uncertainty - PIMCO, accessed March 2, 2026, https://www.pimco.com/gbl/en/insights/bend-not-break-investing-in-real-estate-amid-economic-uncertainty

- 2026 Valuation & Advisory North American Market Survey | Newmark, accessed February 23, 2026, https://www.nmrk.com/insights/market-report/2026-valuation-advisory-north-american-market-survey

- 2026 Commercial Real Estate Trends - J.P. Morgan, accessed March 2, 2026, https://www.jpmorgan.com/insights/real-estate/commercial-real-estate/commercial-real-estate-trends

- Global private markets in real estate - McKinsey, accessed March 1, 2026, https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report/real-estate

- 2025 Retail Rent Dynamics - CBRE, accessed March 2, 2026, https://www.cbre.com/insights/reports/2025-retail-rent-dynamics

- The Enduring Allure of Premier Retail Streets in the Americas | US ..., accessed April 2, 2026, https://www.cushmanwakefield.com/en/united-states/insights/enduring-allure-of-premier-retail-streets

- Emerging Trends in Real Estate: Global 2026 - PwC, accessed April 2, 2026, https://www.pwc.com/gx/en/industries/financial-services/assets/uli-emerging-trends-global-report-2026.pdf

- The Trend Report 2026 by cbgloballuxury - Issuu, accessed February 23, 2026, https://issuu.com/cbgloballuxury/docs/the_trend_report_2026

- 2026 Luxury Outlook Report - Log in | Switzerland Sotheby's International Realty - agence immobilière, accessed April 2, 2026, https://assets.switzerland-sothebysrealty.ch/sites/default/files/2026-01/2026%20Luxury%20Outlook%20Report_compressed.pdf

- Fifth Avenue's annual retail rent of $3,500 per square foot is worl - ICSC, accessed April 2, 2026, https://www.icsc.com/news-and-views/icsc-exchange/fifth-avenues-annual-retail-rent-of-3500psf-is-worlds-highest-report

- Miami's Design District Emerges as a Luxury Retail Powerhouse - CRE Daily, accessed January 2, 2026, https://www.credaily.com/briefs/miamis-design-district-emerges-as-a-luxury-retail-powerhouse/

- Chicago Retail Shines in Neighborhoods, Suburbs - REBusinessOnline, accessed April 2, 2026, https://rebusinessonline.com/chicago-retail-shines-in-neighborhoods-suburbs/

- Why your EBITDA is about to change in 2026 - BKL, accessed April 2, 2026, https://bkl.co.uk/insights/why-your-ebitda-is-about-to-change-in-2026/

- FRS 102 Changes: 6 Ways They Might Impact Your Business - AAB, accessed April 2, 2026, https://aab.uk/blog/frs-102-changes-6-ways-they-might-impact-your-business/

- Does LVMH Own Beverly Hills? A $1B Real Estate Power Play Says Yes https://luxuryretailmarket.org/does-lvmh-own-beverly-hills/

- Kering and Ardian finalize a joint venture agreement for a landmark New York property, accessed April 2, 2026, https://www.kering.com/en/news/kering-and-ardian-finalize-a-joint-venture-agreement-for-a-landmark-new-york-property/

- Kering and Ardian sign $900 million deal on New York's Fifth Avenue - CoStar, accessed January 2, 2026, https://www.costar.com/article/1315313044/kering-and-ardian-sign-an-extraordinary-new-deal-on-new-yorks-5th-avenue

- Acquisition of prestigious Fifth Avenue property in New York City | Kering, accessed February 23 2026, https://www.kering.com/en/news/acquisition-of-prestigious-fifth-avenue-property-in-new-york-city/

- Kering Sells Majority Stake in Fifth Avenue Retail for US$690M - Connect CRE, accessed March 2, 2026, https://www.connectcre.com/stories/kering-sells-majority-stake-in-fifth-avenue-retail-for-us690m/

- Why Luxury Shopping Is Getting Even More Exclusive - Fashionista, accessed February 23 2026, https://fashionista.com/2023/08/private-shopping-experiences-salons-luxury-fashion-brands

- The State of Fashion: Luxury - McKinsey, accessed February 23 2026, https://www.mckinsey.de/~/media/mckinsey/locations/europe%20and%20middle%20east/deutschland/news/presse/2024/2025-01-14%20state%20of%20luxury/the-state-of-fashion-luxury-vf.pdf

- Observations from the rise of independent fashion boutiques - The NuORDER Blog, accessed April 2, 2026, https://blog.nuorder.com/observations-from-the-rise-of-independent-fashion-boutiques

- Catherine Bloom, accessed February 23 2026, https://www.catherinebloom.com/

- Inside Catherine Bloom's Exclusive New Styling Destination at Nordstrom - Modern Luxury, accessed April 2, 2026, https://www.modernluxury.com/catherine-bloom-nordstrom/

- KIMITAKE Now Available in Catherine Bloom for Nordstrom, accessed February 23 2026, https://kimitakejewelry.com/blogs/news/kimitake-now-available-in-catherine-bloom-for-nordstrom

- about the store - EARL IRL, accessed April 2, 2026, https://www.earlirl.com/about

- Beauty and Fashion in 2025: What Really Mattered and What Will Shape 2026, accessed April 2, 2026, https://www.retailtouchpoints.com/executive-viewpoints/beauty-and-fashion-in-2025-what-really-mattered-and-what-will-shape-2026/156322/

- News | Dealmaking projected to double on Chicago's Michigan Avenue in 2026 - CoStar, accessed April 2, 2026, https://www.costar.com/article/1111972849/magnificent-year-of-retail-leasing-projected-for-chicagos-michigan-avenue

- Dallas Retail Market Report Q3 2025 - Matthews Real Estate Investment Services, accessed February 23 2026, https://cms.matthews.com/wp-content/uploads/2025/10/Dallas-Retail-Market-Report-Q3-2025.pdf

- Highland Park, TX Retail Spaces for Lease | LoopNet, accessed April 2, 2026, https://www.loopnet.com/search/retail-space/highland-park-tx/for-lease/